Introduction: The Quiet Revolution Beneath BFSI Modernization

Over the last decade, BFSI institutions and emerging financial technology companies have transformed their relationship from adversaries to powerful collaborators, driving mutual growth. At the heart of this evolution is an unsung hero: Banking Middleware 2.0. Far more than just a technological advancement, Banking Middleware 2.0 is reshaping how financial institutions modernize, integrate, and stay competitive in a fast-paced digital world.

The Legacy Bottleneck: Why Middleware Needed Reinvention

Most BFSI institutions operate on legacy systems built a few decades ago. These systems are stable but rigid, designed for batch processing, not real-time, API-driven Financial Services.

Research shows:

- Many BFSI institutions still use core systems from the 1980s and 1990s, creating a maze of translators and custom connectors to support modern applications.

- This complexity often stretches integrations from weeks to months, slowing time-to-market and inflating costs.

- Even basic customer updates still rely on overnight batch jobs, creating lag and limiting digital experiences.

Traditional integration, point-to-point, bespoke, and slow, can no longer support the speed demanded by digital customers and evolving regulations.

What Is Banking Middleware 2.0?

Banking Middleware 2.0 represents a complete rethinking of financial integration infrastructure. It is:

- API-first rather than core-first

- Event-driven rather than batch-driven

- Cloud-native instead of siloed

- Composable, not monolithic

In simple terms, it acts as a translation and orchestration engine, enabling BFSI institutions’ legacy systems to communicate in real time, without a full overhaul, with new-age, API-driven technology platforms.

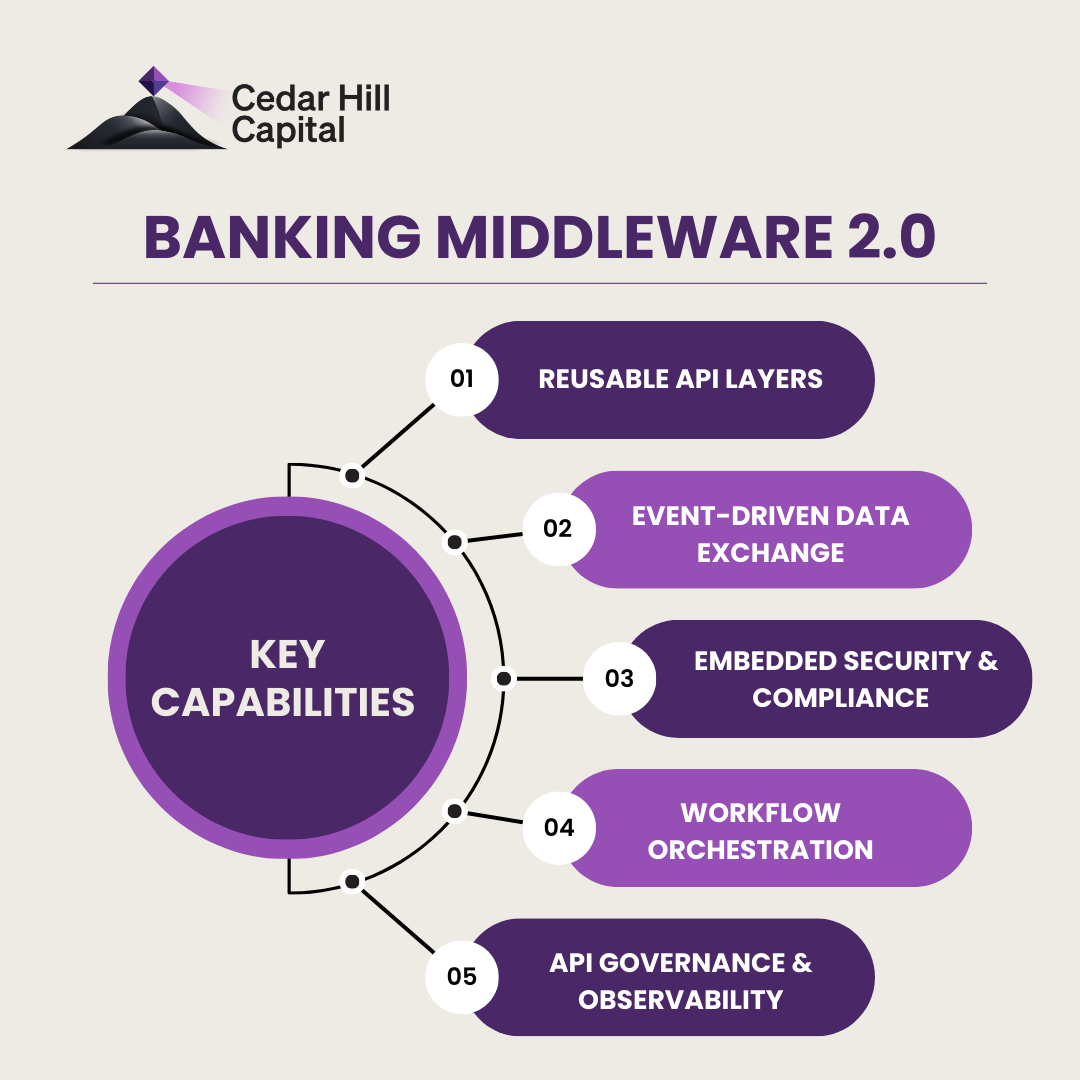

Key capabilities include:

- Reusable API layers: Reusable services for KYC, payments, credit checks, and onboarding, allowing rapid product launches.

- Event-driven data exchange: Instant notifications for payments, transactions, fraud flags, and compliance checks.

- Security and compliance embedded at integration points: Ensuring every consumer of banking data adheres to regulatory norms.

- Workflow orchestration: Routing decisions across services, vendors, or risk engines, crucial for lending, onboarding, and fraud prevention.

- API governance and observability: Real-time monitoring, throttling, traffic management, and versioning, critical in BFSI environments.

The Data Validates the Momentum

Open banking and API-led architectures are no longer future concepts, they are mainstream.

- Global open banking API calls are projected to hit 580 billion by 2027, up from 102 billion in 2023, a 5.6x increase in four years.

- The FinTech market is forecast to reach $699 billion by 2030, driven heavily by API-enabled integrations.

- A growing number of organizations now identify APIs as a top technology priority for digital transformation. As the financial ecosystem becomes more interconnected, Banking Middleware 2.0 is no longer just a technical solution, but a strategic cornerstone for innovation. By enabling BFSI institutions to modernize without overhauling legacy systems, Middleware 2.0 accelerates digital transformation, strengthens security, and ensures scalability. The future of banking is modular, composable, and driven by seamless integration, and Banking Middleware 2.0 is the engine powering that change.